SMM Webinar on aluminium market forecast

With 2019 drawing to a close, Shanghai Metals Market (SMM) presents a series of webinars on the non-ferrous metals market forecast in 2020. Our analysts will share their insights on what’s trending in the non-ferrous metals Chinese domestic markets, as well as providing their analysis on the fundamentals that affects demand and supply.

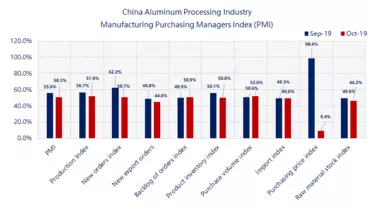

What’s trending in the Chinese domestic aluminium market?

Production of primary aluminium in China is expected to grow much faster than consumption in 2020. According to SMM senior aluminium analyst Lucy Liang, stronger supply pressure is weighing on aluminium prices in the coming year.

“Output of primary aluminium in China is estimated to increase 2.5% to 36.44 million tonnes next year, after shrinking 1.51% this year. Aluminium consumption in China will also pick up, albeit at a much slower pace of 0.3% to 36.19 million tonnes, from a decline of 1.48% in 2019,” he said at the recent China Nonferrous Metals Industry Annual Meeting 2019.

Liang added: “With 1.99 million tonnes of capacity online in the first ten months of the year, there was 40.69 million tonnes of primary aluminium capacity built in China as of the end of October on an annualised basis, and 35.1 million tonnes was in operation.”

SMM data showed that social inventories of primary aluminium ingots, including SHFE warrants, have fallen below 800,000 tonnes, due to limited arrivals and decent consumption. Supply pressure looks underwhelming in the short term, in anticipation of limited capacity expansion as Chinese smelters put off the resumption of idled facilities.

From a long-term perspective, fundamentals are deteriorating as the latest SMM survey showed that aluminium downstream consumption in November to December is weakening from the traditional high season September and October.

On the other hand, alumina capacity expansion in China and technical upgrading are set to maintain imports of bauxite at high levels in 2020, but the growth will be slower.

<strong>Webinar focus

- How cash flows, local subsidies and profitability will impact the commissioning schedule of aluminium smelters in China

- Updated forecast of operating capacity changes of aluminium smelters in China from Q4 in 2019 to Q1 in 2020

- How the importing of bauxite and alumina will make a difference in alumina production cost and profitability in China

- Forecast of operating capacity changes of alumina refineries in China from Q4 in 2019 to Q1 in 2020

Webinar Details

Date/Time: Thu. Dec 5,2019 4:00 PM CST

An analysis of the worldwide aluminium market at the turn of 2023/24 and an outlook for the year 2024.

Ideally suited for aluminium, copper and non-ferrous alloys, green sand casting can produce castings in low, medium or high volumes in varying sizes, to meet the specific requirements of foundries.

With the acquisition of GIC Magnet, Ducab Metals Business aims to expand its range of products and strengthen its position in the global market.